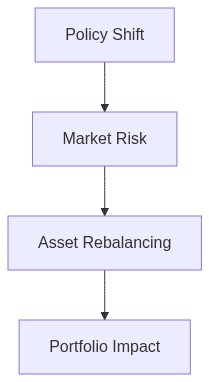

- The yen carry trade has supported low-cost global investments, particularly in commercial real estate, but unwinding is increasing borrowing costs.

- Increased global equity volatility is affecting real estate asset valuations, leading to potential repricing of assets and affecting investor sentiment.

- In the face of rising interest rates and currency fluctuations, commercial real estate transactions are witnessing delays as investors recalibrate strategies.

- Institutions must consider hedging strategies and portfolio diversification to navigate the volatility unleashed by yen carry trade unwinding.

- Adaptive strategies in real estate investment are crucial due to evolving financial conditions and geopolitical uncertainties linked to global market shifts.

“In macro investing, being early is indistinguishable from being wrong. Timing is the ultimate alpha.”

Macro-Economic Context & Structural Imbalances

In the turbulent sea of global finance, the yen’s recent unwinding has emerged as a linchpin in market dynamics, with profound implications reverberating across the real estate sector. The yen carry trade, a leveraged strategy capitalizing on low Japanese interest rates, has begun its much-feared unwinding. This reversal is precipitated by shifts in Japan’s monetary policy and increasing yield attractiveness elsewhere, notably in the United States. Japan’s stance amidst the recalibration of its inflationary outlook is seen as a beacon on how central bankers worldwide might navigate the vast ocean of liquidity manipulation.

Structural imbalances set the stage investors are recalibrating their holdings amid increasing yen volatility, causing significant ripple effects through real estate markets. The notable surge in yen appreciation, linked directly to the unwinding, confronts a global economic environment fraught with uncertainty and risk. As the Bank of Japan cautiously adjusts its policy angles, foreign exposure and multinational real estate investments feel the gravitational pull of changing exchange rate dynamics. Despite historically low interest rates that have fueled asset bubbles, the pendulum’s recent swing highlights notable vulnerabilities in the system.

“The volume of yen-carry trade positions has swollen due to ultra-low Japanese interest rates; its sudden detonation could spark price volatilities in vulnerable global markets.” – IMF

Quantitative Impact on Asset Pricing

The yen’s appreciation has a direct quantitative effect on asset pricing through fundamental and technical lenses. From a fundamental perspective, increased funding costs and negatively skewed risk-reward equations exert deflationary pressures on the Japanese economy, diluting real estate value appreciation. Simultaneously, baseline quant models suggest a distinct support level breach, adding technical headwinds to the structural economy.

The inverse liquidity premium becomes palpable as capital retreats from risk-laden asset classes. Recovery curves display convexity deflation, indicating stressed portfolio thresholds. In the context of real estate, the traditionally unwavering capital influx faces drought conditions due to an altered risk appetite among elite investors. Tail-risk amplification appears imminent as valuation corrections align with broader macro risks, furthered by yen bullishness.

“Global financial conditions have tightened, as evidenced by rising debt spreads and a palpable shift in market sentiment, which augurs poorly for liquidity-sensitive sectors such as real estate.” – BIS

Step 1 Asset Class Allocation

Enhance allocation towards higher-yield alternatives with mature markets that present limited currency risk exposure. European real estate, fortified by a steadfast euro and low liquidity premia, presents a viable outlet amidst yen disturbances. Underweight Japanese estate interaction cautiously, maintaining vigilant short-duration hedges.

Step 2 Risk Mitigation & Hedging

Implement risk mitigation strategies through judicious use of derivatives, creating asymmetric hedging structures to offset potential downside. Currency forwards and options offer a safeguard against unanticipated yen appreciation. Furthermore, integrate credit default swaps where warranted to bolster position stability amidst fluctuating debt markets.

Step 3 Tactical Gains Exploitation

Recalibrate tactical responses to capture ephemeral pricing mismatches, exploiting volatility induced convexity merits. Enter into calculated positions relating to regional REITs with favorable fiscal outlooks outweighing translational effects. Use time-decayed options to strategically gain exposure without systemic risk escalation.

Final Thoughts

As we stand at the intersection of historic financial intricacies, determining the path forward necessitates a calculated, data-driven approach. With tailwinds of change evident in the yen sensitivity, establishing future-proof investment strategies is crucial for maintaining portfolio integrity while maximizing alpha. Our directive remains potent and fiercely analytical, designed to navigate the tumult close on the horizon.

| Feature | Retail Approach | Institutional Overlay |

|---|---|---|

| Objectives | Maximize individual asset returns | Optimize portfolio-level risk-return balance |

| Data Utilization | Limited financial data and indicators | Comprehensive data analytics and macroeconomic indicators |

| Risk Management | Basic risk assessment tools | Advanced models incorporating geopolitical shifts and currency fluctuations |

| Yen Exposure | Direct currency impact on investments | Hedging strategies to mitigate currency risk |

| Real Estate Focus | Specific property assets | Asset-backed securities and REITs for diversification |

| Decision-making | Based on market sentiment and trends | Algorithmic trading models and predictive analytics |

| Capital Allocation | Individual stakeholders determine investments | Strategic asset allocation across multiple sectors |

| Market Analysis | Simplified market overviews | In-depth market analysis and economic forecasts |

| Liquidity Management | Focus on short-term liquidity | Long-term liquidity planning with stress tests |