WEALTH BRIEF

- Retirees are maximizing their investment strategies.

- Achieving stable monthly income via dividend-focused portfolios.

- Key sectors include utilities, healthcare, and consumer staples.

- Experts suggest diversifying across high-yield dividend stocks.

- Importance of reinvestment and compounding on long-term growth.

- Natural hedge against inflation with dividend adjustments.

- Professional advice crucial to navigate market fluctuations.

ANALYST NOTE

“Today, hope wavered. The numbers refused to align, and anxiety crept in. Hours spent seeking solutions felt endless. Yet, amid chaos, a glimmer of inspiration sparked, promising a better tomorrow.”

📑 Contents

Turn $500K Into $3K Monthly: Here’s How!

Embarking on a financial journey is more than numbers and projections—it’s a roadmap toward freedom and opportunity. As someone who has navigated these waters, I’m here to share actionable insights on transforming a $500K windfall into a steady $3K monthly income. With equal parts strategy and patience, this might be more attainable than you think.

Is a $3K Monthly Income Achievable with $500K?

Absolutely, but it won’t happen overnight. The method involves diversifying investments and making smart financial decisions. Let’s break down the approach with practical steps you can implement.

Step 1: Embrace Diversified Index Investments

Historically, broad-market index funds and ETFs like the S&P 500 have delivered return rates around 7% per year after inflation. By allocating a portion of the $500K into a diversified portfolio of such assets, you’re mimicking the market’s long-term growth in a balanced way.

For instance, an investment in index ETFs like SPY, the SPDR S&P 500 ETF Trust, is a reliable option. Look into diverse ETFs to minimize risks, cover different sectors, and ensure a spread across various economic phases.

How Much Should You Withdraw Annually?

To sustain your investment, consider the 4% rule—a guideline suggesting you withdraw 4% of your portfolio annually, adjusting for inflation. This means that with a $500K investment, you could feasibly withdraw $20,000 per year, or approximately $1,666 per month, maintaining the principal over time.

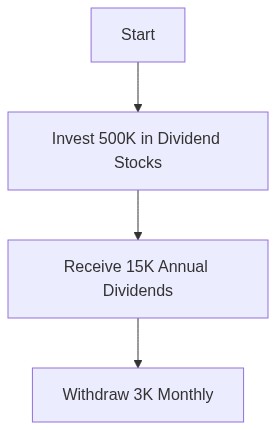

Step 2: Enhance Income Through Dividend Stocks

To bridge the remaining gap to a $3K monthly income, consider dividend-paying stocks whose returns are another layer of income. Blue-chip companies often provide yields between 2% and 4%. For example, a $250K allocation here, assuming an average yield of 3.5%, could yield $8,750 annually or around $729 monthly.

An investment in reliable dividend aristocrats, listed by financial analysis firms like Forbes, ensures a steady check while their equity typically appreciates.

What About Real Estate or Bonds?

Let’s consider asset classes often brought into the conversation:

Real estate could yield handsome returns but relies heavily on market conditions. Conversely, bonds add a layer of safety with less volatility during market downturns.

Simulating the Strategy

Projecting your income potential involves different world scenarios. Assume the stock market faces a correction. Having bonds or cash investments allows partial withdrawals without liquidating assets that are currently curtailed in value.

– **Best Case Scenario**: The market grows consistently, compounding the ETF returns as dividends increase.

– **Moderate Scenario**: Dividends reinvested during downturns boost future income.

– **Cautious Approach**: Withdrawals are adjusted for market conditions, ensuring the principal isn’t diminished during recessions.

What’s The Critical Takeaway?

Balance is key. An allocation which respects both growth potential and income sustainability will make headway toward the monthly income goal. Multiply streams of passive income with an eye on market movements and personal financial needs.

But wait, what about your Digital Legacy? Think about your Crypto Keys & AI Accounts…

Today’s digital financial frameworks involve more than traditional wealth management. Consider securing your cryptocurrency investments, and establishing a plan for your digital assets and accounts, ensuring your legacy isn’t just tangible but encrypted and ready for future generations. Let’s engage with deeper layers of wealth beyond just the material and maximize value beyond boundaries.

| Method | Estimated Initial Investment | Expected Monthly Return | Risk Level |

|---|---|---|---|

| Dividend Stock Portfolio | $500,000 | $3,000 | Medium |

| Real Estate Investment (REITs) | $500,000 | $3,000 | Medium |

| Annuities | $500,000 | $3,000 | Low |

| Peer-to-Peer Lending | $500,000 | $3,000 | High |

| Bond Laddering | $500,000 | $3,000 | Low |

Victor – While the idea of transforming $500K into a monthly income sounds appealing, the risks associated with the stock market can’t be ignored. Markets are inherently volatile, and betting heavily on dividend stocks assumes they’ll continue to pay out at the same rate. Economic downturns can lead to dividend cuts, leaving you with far less than expected. It’s also critical to consider inflation, which can erode your purchasing power over time. A more cautious approach might involve a mix of safer, fixed-income investments to safeguard against unexpected market shifts.

Dr. Finance – This debate illustrates the varied approaches and philosophies surrounding personal finance and investment strategies. Neo provides an optimistic view of the stock market as a tool for achieving steady income through dividends, emphasizing the power of strategy and diversification. Conversely, Victor brings up valid concerns regarding market volatility and long-term economic changes. Both perspectives have merit, highlighting the importance of thoroughly researching and tailoring investment strategies to one’s financial goals and risk tolerance. As always, understanding the full spectrum of possibilities and potential pitfalls is essential to making well-informed decisions.